App Gallery

Detailed Description

Venmo: Streamlined Social Payments for Everyday Life

Venmo is a digital wallet and payment platform that simplifies peer-to-peer transactions by integrating social features. Owned by PayPal, it allows users to send and receive money instantly via a mobile app. Its core innovation lies in combining financial transfers with a social feed, where users can share payment descriptions, fostering transparency and connection. Venmo supports bank transfers, debit cards, and credit cards, making it a versatile tool for splitting bills, paying rent, or sending gifts. With over 90 million users in the United States, it has become a standard for cashless, mobile-first transactions.

Chapter 1: Function

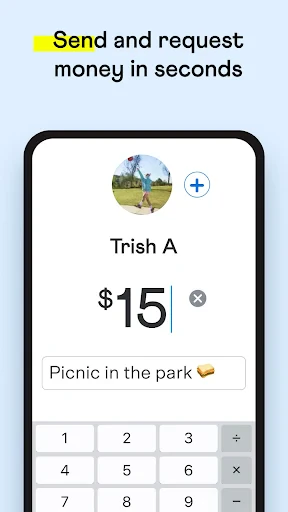

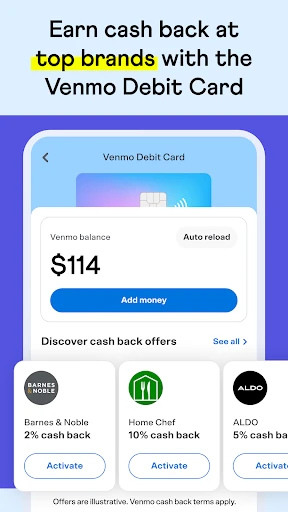

Venmo enables users to send money to any other Venmo user by searching their username, phone number, or email. Funds are drawn from a linked bank account, debit card, or Venmo balance. The app offers instant transfers to bank accounts for a small fee, though standard transfers are free and take one to three business days. Users can request money, split payments among multiple people, or set up recurring payments. A unique social feed shows transactions publicly by default, allowing friends to like or comment on payments, though privacy settings let users hide specific transactions. Venmo also provides a physical or virtual debit card for spending the balance in stores. Additionally, it supports cryptocurrency buying and selling within the app, expanding beyond core payment functionality.

Chapter 2: Value

Venmo’s primary value lies in its seamless integration of social interaction with financial management, transforming mundane money transfers into a lighthearted experience. The social feed encourages transparency among friends and family, reducing awkwardness around repaying debts or splitting shared expenses. Its user-centric design prioritizes speed and convenience: sending money typically requires just a few taps, and the app’s widespread adoption means most interactions are frictionless. Key advantages include zero fees for standard bank transfers, making it cost-effective for everyday use. The request feature empowers groups to divide bills instantly, while the instant transfer option provides critical liquidity in emergencies. Venmo also offers purchase protection for eligible transactions, adding a layer of security. For businesses, Venmo allows merchants to accept payments via QR code or integration, expanding its utility beyond personal use. The platform’s robust privacy controls enable users to balance social sharing with discretion. By blending utility with entertainment, Venmo reduces barriers to digital payments, encouraging even traditionally cash-only users to adopt mobile transactions. Its low barrier to entry, requiring only an email or phone number, ensures broad accessibility.

Chapter 3: Scenarios

Venmo primarily targets millennials and Gen Z users in the United States who are comfortable with mobile technology and seek frictionless financial interactions. Its common use cases include splitting dinner bills among friends, sharing rent or utility costs with roommates, and repaying small loans from acquaintances. Students use it to collect money for group projects or events. Freelancers and gig workers rely on Venmo for quick payments from clients, while parents send allowances to children. The platform also serves small business owners who accept it as a low-cost payment alternative. Everyday scenarios include paying for shared travel expenses, such as hotel rooms or gas, and sending last-minute gifts like birthday cash. Venmo’s social feed also makes it a tool for micro-communities, such as clubs or sports teams, to track payments transparently. During emergencies, users leverage instant transfers for urgent repairs or medical costs. The app’s debit card extends its use to physical retail purchases, enabling users to spend their balance anywhere Mastercard is accepted.

Features & Pros

- transfers cash instantly between users

- social feed shows transaction descriptions publicly

- works with most US bank accounts and cards

- splits bills by tagging friends in payments

- uses bank-level encryption for transaction data

Limitations & Cons

- charges 3% fee for credit card transfers

- requires both sender and recipient to have accounts

- public feed exposes spending habits by default

- limited to US-based bank accounts only

- no option to undo an accidental payment

Frequently Asked Questions

What is Venmo and how does it work?

Venmo is a mobile payment app that allows users to send and receive money directly from their bank accounts or Venmo balance. It works by linking a debit card, credit card, or bank account, then transferring funds to other users via their username, email, or phone number. Transactions can include a note and are shared on a social feed unless set to private. Payments are typically instant or take one business day for standard transfers.

Is Venmo free to use or are there fees?

Venmo is free for sending money from a linked bank account or Venmo balance using a debit card. Credit card transactions incur a 3% fee. Instant transfers to a bank account cost 1% (minimum $0.25, maximum $10). Standard transfers to a bank account are free and take one to three business days. Business or in-app purchases may involve seller transaction fees.

What devices and systems support Venmo?

Venmo is available on iOS (version 13.0 or later) and Android (5.0 or later) smartphones. The app requires internet access and permission to access contacts for sending to friends. It does not support desktop or tablet versions for sending money, though the website allows limited account management. Users must be 18 or older and reside in the United States.

Can Venmo be used for business or commercial transactions?

Venmo offers a separate business profile for merchants to accept payments from customers. Personal accounts are not intended for business sales and may be flagged if used for regular commercial activity. Business profiles incur a 1.9% plus $0.10 fee per transaction. Sending money to businesses requires scanning a QR code or using the business’s username. Refund and dispute procedures differ from personal transactions.

How do I resolve unauthorized transactions or payment issues?

If you notice an unauthorized transaction, report it through Venmo’s in-app support immediately. Venmo offers a purchase protection program for eligible transactions. For failed or incorrect payments, contact the recipient first to request a refund. Venmo’s support team can cancel pending payments. Standard bank disputes should be filed with your card issuer. Venmo does not provide phone support; use the help center in the app.