App Gallery

Detailed Description

Self - Credit Builder: Build Credit with Savings

Self - Credit Builder is a financial technology app designed to help individuals establish or improve their credit scores through a secured savings-based loan model. Unlike traditional credit cards or unsecured loans, this app requires users to make monthly payments into a Certificate of Deposit that serves as collateral. Over time, these payments are reported to major credit bureaus, allowing users to build a positive credit history without taking on high-risk debt. The app offers flexible payment plans, transparent fee structures, and progress tracking tools. It is particularly valuable for those with limited or damaged credit who seek a disciplined, low-risk path to financial credibility.

Chapter 1: Function

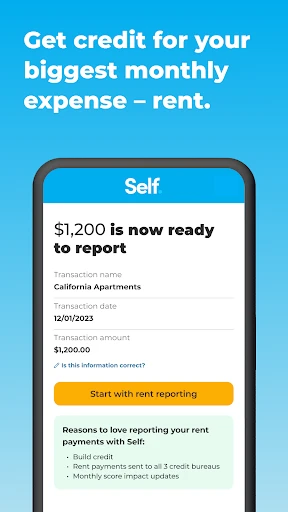

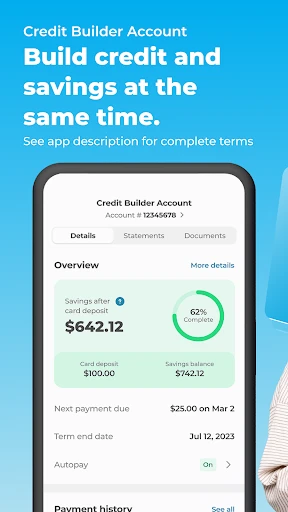

The core function of Self - Credit Builder is to provide a structured savings program that simultaneously builds credit. Users choose a fixed-term loan amount and a monthly payment plan that fits their budget. Each payment is deposited into a secure savings account, and the app reports these on-time payments to all three major credit bureaus: Equifax, Experian, and TransUnion. At the end of the term, users receive the saved funds minus a small administrative fee. The app also offers a linked self Visa credit card for further credit health, which requires a deposit and reports usage to bureaus. Key features include automatic payment scheduling, credit score monitoring through VantageScore, and educational resources to help users understand credit factors. The interface simplifies the complex process of credit building into actionable, automated steps, ensuring users can focus on consistent payments without managing multiple accounts.

Chapter 2: Value

Self - Credit Builder delivers significant value by addressing the core challenge of credit invisibility and poor credit history. Its primary advantage is risk mitigation: because the loan is fully secured by user deposits, there is no chance of accumulating unmanageable debt. This makes it accessible to individuals who may be rejected by traditional lenders due to low scores or no history. The app serves as a forced savings mechanism, rewarding users with both credit improvement and a lump sum of cash at term end. This dual benefit distinguishes it from credit cards that encourage spending or predatory loans that trap users in high interest. Another key advantage is transparency: the app discloses all fees upfront, with no hidden charges or variable interest rates. The monthly reporting to three bureaus accelerates credit building, as consistent payments can yield a 40 to 80 point score increase within six months according to user data. For users who lack the discipline to save independently or the knowledge to navigate credit systems, Self provides a guided, automated solution. It also offers a graduation path to unsecured products, such as the self Visa card, which can further expand credit access. Ultimately, the app transforms financial exclusion into inclusion by proving creditworthiness through savings behavior rather than income or existing credit lines. This makes it a powerful tool for students, recent immigrants, and those recovering from bankruptcy or financial setbacks.

Chapter 3: Scenarios

The primary target users include young adults with no credit history, such as college students or recent graduates just entering the financial system. For example, a student with no credit cards can start with a 25 monthly plan to establish a file. Another key group is individuals with poor credit scores, such as those who have defaulted on loans or declared bankruptcy. These users can use Self as a rehabilitation tool to demonstrate responsible payment behavior over 12 or 24 months. Immigrants new to the United States also benefit, as they can build a U.S. credit profile from scratch without needing a Social Security number or existing history. Everyday use cases include setting up automatic payments linked to a checking account and monitoring credit score changes monthly. For freelancers or gig workers with irregular income, the fixed payment schedule encourages financial discipline. The app is also used by parents wanting to teach teenagers about credit management in a low-risk environment. In each scenario, the user pays down a secured loan over time, and the app handles all reporting and educational outreach, minimizing complexity.

Features & Pros

- incognito credit checks won’t ding your score

- uses rent and utility payments to build history

- no hard pull for initial account setup

- provides real-time FICO 8 tracking monthly

- deposit-free secured card for credit limits

Limitations & Cons

- requires regular income verification to activate

- limited to US citizens with valid SSN

- annual fee up to $25 cuts into small limits

- no joint or authorized user option available

- mobile app lacks budgeting tools for spending

Frequently Asked Questions

What is Self - Credit Builder and how does it work?

Self - Credit Builder is a financial app categorized under credit building tools. Its core function is to help users establish or improve credit scores through a secured installment loan model. Users select a savings goal amount, pay an initial deposit, and then make monthly payments toward that goal. These payments are reported to all three major credit bureaus (Equifax, Experian, TransUnion). After completing the term, users receive the saved amount back minus fees. No credit check is required to start.

Is Self - Credit Builder free to use or are there in-app purchases?

Self - Credit Builder is not free. It requires a mandatory initial deposit (typically $25 or $50) and monthly administrative fees ranging from $4 to $15 per term depending on the chosen plan. There are no additional in-app purchases for core functionality, but users cannot skip payments. The app operates on a prepaid loan model, meaning all fees are disclosed upfront before enrollment. No hidden costs are associated with the basic service.

Does Self - Credit Builder require a specific device or system version?

Self - Credit Builder is compatible with iOS devices running iOS 13.0 or later and Android devices with OS 6.0 or later. The app requires a stable internet connection for account management and payment processing. It does not require any external hardware or additional equipment. The app is designed for individual users with a valid Social Security Number (SSN) or Individual Taxpayer Identification Number (ITIN) in the United States.

Can I cancel my Self - Credit Builder plan early without penalty?

Yes, users can cancel their Self - Credit Builder plan at any time without a cancellation penalty. However, early cancellation means the user forfeits the initial deposit and any saved funds will be returned minus the deposit and fees already paid. The credit reporting history from completed payments remains on the credit report only if the plan is fully paid. Partial payments may not be reported as positive history.

How long does it take to see a credit score improvement with Self - Credit Builder?

Self - Credit Builder reports payment activity to the credit bureaus every 30 days, with the first report typically appearing within 45 to 60 days of enrollment. Users may see a credit score increase within 3 to 6 months if payments are made on time. The degree of improvement depends on individual credit profiles, such as starting score, existing account mix, and payment history. The app does not guarantee specific score results.