Kikoff - Build Credit Quickly

FinanceKikoff helps build credit fast for credit newbies seeking a simple starter loan.

App Gallery

Detailed Description

Kikoff - Build Credit Quickly: Your Path to a Stronger Credit Profile

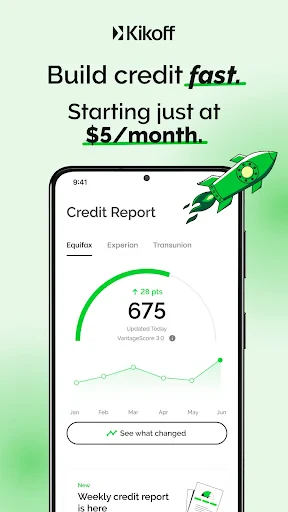

Kikoff is a financial technology application designed to help users establish and improve their credit scores from scratch or after a financial setback. Unlike traditional credit cards or loans, Kikoff offers a unique approach by providing a Credit Builder Account that functions like a no-interest installment loan. The app reports payment activity to the three major credit bureaus Equifax, Experian, and TransUnion, enabling users to build a positive credit history with minimal financial risk. Its core premise is simplicity and accessibility, targeting individuals who are credit invisible or have thin credit files.

Chapter 1: Function

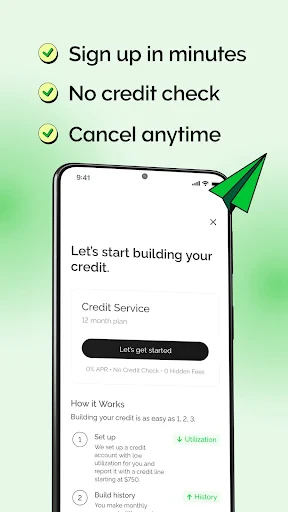

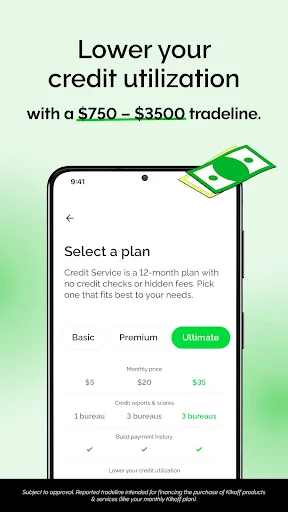

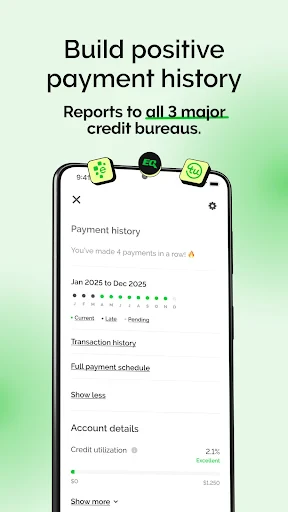

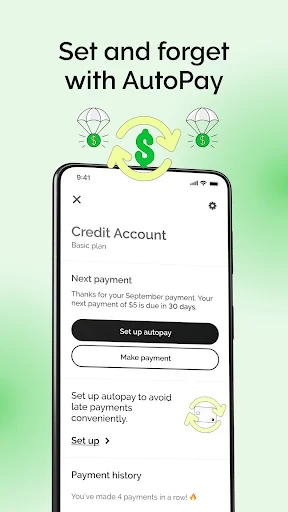

Kikoff’s primary function is to create a new credit history through a simple, low-cost credit builder loan. The process begins when a user selects a credit limit, typically between 10 and 100 dollars. Kikoff then deposits this amount into a secured savings account held in the user’s name. Instead of requiring an upfront payment, the user agrees to make 12 monthly payments equal to one-twelfth of the chosen credit limit. For example, a 100 dollar credit limit results in 12 monthly payments of approximately 8.33 dollars. Kikoff reports these on-time payments to the credit bureaus each month, effectively building a positive payment record. The app also offers a secured credit card feature for further credit building, though the core function remains the installment loan model. Users manage everything through the mobile app, which provides a clear dashboard showing payment schedules, credit limit, and progress reports. The key functional advantage is that the user pays the loan back to themselves over time, as the funds are held in a non-withdrawable savings account until the loan term ends, minimizing risk and cost.

Chapter 2: Value

The primary value proposition of Kikoff lies in its low-risk, high-accessibility approach to credit building. For individuals with no credit history, often referred to as credit invisible, or those recovering from poor credit, traditional credit products like unsecured credit cards or personal loans are frequently inaccessible due to stringent approval requirements. Kikoff bypasses this barrier entirely by not performing a hard credit inquiry at signup, meaning users can start building credit without further damaging their score. The financial risk is minimal because the user is essentially paying a small monthly amount that is returned to them at the end of the 12-month term, minus a small membership fee, resulting in a net savings of around 96 percent of the principal. This models teaches financial discipline while simultaneously reporting positive payment history. A key advantage is the app’s transparent reporting structure. It directly reports to all three major bureaus, providing comprehensive score improvement. Additionally, the secured credit card option offers a further path to credit building by granting a small line of credit that is secured by a refundable deposit. The app’s interface provides clear educational content and progress tracking, empowering users to understand how their actions affect their credit score. For many users, Kikoff represents a first step into the formal credit system, offering a controlled, predictable, and safe environment to establish a positive credit identity, which is crucial for future financial opportunities like renting an apartment, getting a car loan, or lowering insurance premiums.

Chapter 3: Scenarios

Kikoff is primarily designed for individuals with thin or non-existent credit files. The primary target user group includes young adults, such as college students or recent graduates, who have never held a credit card or loan and need to establish a baseline credit history. Another significant user group is immigrants who have recently moved to the United States and possess strong credit histories in their home countries but have no U.S. credit records, a situation known as being credit invisible. A third key group consists of individuals who have experienced past credit challenges, such as bankruptcy, foreclosure, or a series of late payments, and are now seeking a stable and safe method to rebuild their credit profile without risking large sums of money. In everyday use, a typical scenario involves a student opening the app, selecting the 10 dollar credit builder plan, and setting up automatic monthly payments to ensure consistent on-time reporting. Another common use case is an individual using the Kikoff secured credit card for small, regular purchases like a monthly streaming subscription, which is then paid off in full each month, demonstrating responsible credit utilization. The app serves as a foundational tool in a broader financial health strategy, often used in conjunction with other products like secured credit cards from major banks or rent reporting services, allowing users to layer multiple positive credit building activities.

Features & Pros

- loans reported to all 3 bureaus monthly

- no hard credit pull for account opening

- credit line grows with on-time payments

- low minimum deposit to start

- spending limit increases without extra fee

Limitations & Cons

- requires upfront deposit as collateral

- credit line limited to store spend only

- no cash back or rewards on purchases

- APR can be high on carried balances

- limited consumer protections vs traditional card

Frequently Asked Questions

What does Kikoff do for credit building?

Kikoff offers a credit-building service through a no-fee credit line that reports to major credit bureaus. Users make monthly payments on small purchases, which are reported to Experian, Equifax, and TransUnion to help establish or improve credit scores. No credit check is required to start.

Is Kikoff free to use or are there hidden fees?

Kikoff charges no interest or hidden fees for its core credit-building feature. However, optional subscriptions like Credit Monitoring Plus may have monthly costs. There are no in-app purchases required for basic functionality, and no additional equipment is needed beyond a smartphone.

How does Kikoff report to credit bureaus?

Kikoff reports your monthly account status to all three major credit bureaus: Experian, Equifax, and TransUnion. On-time payments and low credit utilization are reported, similar to a traditional credit card. Negative activity like late payments may also be reported, impacting your score.

Can Kikoff help if I have no credit history?

Yes, Kikoff is designed for users with no or limited credit history. It requires no credit check to open an account and builds history through small, consistent payments. Initial credit lines start at around $750, and users typically see a FICO score within 2–4 months after first payment reporting.

Does Kikoff work with all US mobile devices?

Kikoff is available on iOS and Android devices via the official app stores. It requires an active US phone number and Social Security Number for identity verification. The app is not available outside the United States, and there is no web-based account management besides the mobile interface.