App Gallery

Detailed Description

Four: Buy Now, Pay Later – Flexible Payment for Modern Shopping

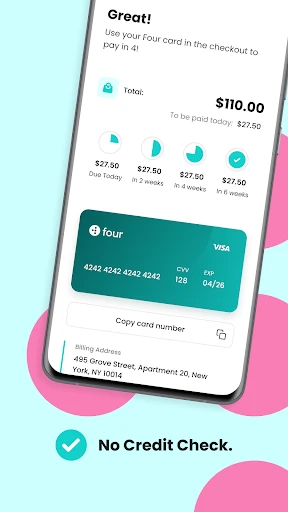

Four is a digital financial application that enables users to split their purchases into four interest-free installments, payable every two weeks. Designed for both online and in-store transactions, the app integrates seamlessly with major retailers and e-commerce platforms. Users can create an account, link a debit or credit card, and instantly apply this payment method during checkout. The service requires only a soft credit check for eligibility, making it accessible to a broad audience. By deferring payment without accruing interest, Four addresses the need for short-term liquidity while avoiding traditional credit card debt cycles. The app also includes features such as purchase tracking, payment reminders, and a digital wallet for managing multiple installment plans simultaneously. Its focus on transparency, no hidden fees, and immediate approval distinguishes it in the buy-now-pay-later market.

Chapter 1: Function

Four’s core functions revolve around providing instant, interest-free installment credit. Upon installing the app, users undergo a quick verification process that assesses their financial standing through a soft credit pull. Once approved, they receive a spending limit tied to their account. During online checkout, users can select Four as their payment option, initiating a four-payment schedule: the first 25 percent is due immediately, with the remaining three payments deducted automatically from the linked card every two weeks. For in-store purchases, the app generates a digital card that can be added to mobile wallets like Apple Pay or Google Pay. Additionally, the dashboard displays all active plans, upcoming due dates, and remaining balances. Users can also adjust payment dates or prepay remaining balances without penalty. The app integrates with over 10,000 merchants globally, spanning categories such as fashion, electronics, home goods, and travel. Notably, Four does not charge late fees or service fees, setting it apart from competitors that impose penalties for missed payments.

Chapter 2: Value

The primary value of Four lies in its ability to enhance purchasing power without the burden of interest or long-term debt. Traditional credit cards often carry annual percentage rates exceeding 20 percent, whereas Four’s zero-interest model ensures that users pay exactly the listed price, split into manageable chunks. This structure benefits budget-conscious consumers by aligning payment schedules with biweekly pay cycles, reducing financial strain. Furthermore, the soft credit check eliminates the risk of damaging credit scores through hard inquiries, making it suitable for individuals with limited or recovering credit histories. From a psychological standpoint, the app reduces the pain of a large one-time expense by distributing it over six weeks, encouraging responsible spending. For merchants, Four drives higher conversion rates and average order values, as customers are more likely to complete purchases when payments are broken down. The app also promotes financial inclusion by providing access to credit for those who may not qualify for traditional cards. Comparative analysis shows that Four’s no-fee policy saves users an average of 30 percent in ancillary costs versus similar services. Additionally, the app’s transparency regarding terms and conditions builds trust, while automatic payment reminders prevent accidental defaults.

Chapter 3: Scenarios

Four targets a diverse user base, including millennials and Gen Z consumers who prioritize flexibility and avoid long-term debt. Young professionals, for instance, use the app to purchase work attire or electronics during salary gaps, as the biweekly schedule aligns with paydays. College students benefit from splitting textbook or laptop costs without incurring credit card debt. Families leverage Four for larger household purchases like furniture or appliances, maintaining cash flow between paychecks. Freelancers and gig economy workers, who face irregular income streams, use the app to smooth out essential expenses. In everyday scenarios, a user might choose Four for a 200-dollar pair of sneakers, paying 50 dollars immediately and 50 dollars every two weeks. Similarly, a traveler can book a 400-dollar flight, paying installments over six weeks without interest. The app also supports impulse purchases, such as holiday gifts or event tickets, where the psychological barrier of a large upfront cost is lowered. Retailers in fashion and electronics see peak usage during Black Friday and back-to-school seasons. For in-store experiences, users at partner stores like clothing boutiques can scan a QR code to generate a payment plan at the register. Four’s integration with online checkout ensures compatibility with major platforms like Shopify and WooCommerce, covering both digital and physical goods.

Features & Pros

- instant credit approval for purchases under 30 seconds

- no interest if paid within 14-day grace period

- works with any merchant that accepts Visa or Mastercard

- real-time spending limit adjustment based on purchase history

- automatic payment deduction from linked bank account

Limitations & Cons

- late fees start after just 3 days overdue

- credit limit starts at only $200 for new users

- no integration with popular e-wallets like PayPal or Apple Pay

- requires a credit check

- impacting score temporarily

- app unavailable in 12 US states due to regulatory restrictions

Frequently Asked Questions

What is Four and how does it work?

Four is a Buy Now, Pay Later app that lets you split purchases into four equal interest-free payments. You pay 25% upfront, then the remaining three payments are automatically charged every two weeks. It works at any store that accepts Visa or Mastercard, both online and in-store, via a virtual card in the app. No interest or fees if paid on time.

Does Four require a credit check or a bank account?

Four performs a soft credit check during sign-up, which does not affect your credit score. You need a valid debit or credit card to link to your account for payments. A bank account is not required, but your linked card must have sufficient funds to cover each installment. Minors or users without a government-issued ID cannot sign up.

What are the fees if I miss a payment?

If you miss a payment, Four charges a late fee of up to $8 per missed installment, depending on your state’s regulations. There are no interest charges or service fees for on-time payments. The app sends reminders before each due date to help avoid late fees. You can also reschedule a payment once per order via the app.

Can I use Four for any purchase and with any merchant?

Four can be used for purchases ranging from $30 to $1,000 at any merchant that accepts Visa or Mastercard, both online and in physical stores. Excluded categories include money transfers, gambling, and prepaid cards. The app provides a digital card number that you add to Apple Pay or Google Pay for contactless in-store use.

How do I return an item purchased with Four?

To return an item, follow the merchant’s standard return policy. Once the merchant processes your refund, Four automatically adjusts your remaining payments. If the refund covers the full purchase, all pending installments are canceled and the amount you paid upfront is returned to your original payment method, typically within 5–10 business days.